Is your laboratory looking for ways to save money? Try spending (investing) some!

This idea seems counterintuitive, doesn’t it? The traditional approach to cutting expenses has always been just that—cutting. Very few laboratories will even consider the idea that they can spend, actually invest, their way to an improved bottom line. Yet there are opportunities to make cost-saving improvements if you look in the right places. Over the past 20 years of visiting testing labs in nearly every industry, we have noticed a common problem— many labs have inefficient processes that are costing them a significant amount of time and money. Sometimes the problem is an old piece of equipment that once was state of the art but now is a few generations behind current technologies. In other cases, you have an outdated procedure. Maybe you developed it 15 years ago, or maybe you were given it by your customer. Either way, it takes too much time and uses too many resources. Finally, in the quest to lower staff costs, companies have lost their experienced laboratory leaders, who used to mentor junior staff on how to do things the right way. We see many labs filled with young, inexperienced analysts, and few who can be resources to them for solving problems. As a result, they make more mistakes or are just less efficient in everything they do, which is not their fault. Most are a joy to work with;they are eager to learn and appreciate the help that we give them, because it makes their jobs easier and reduces their stress levels. Of course, the laboratory benefits as well when its staff are happier and more efficient.

Why don’t more laboratories make an effort to fix these situations? Today’s laboratories face many challenges, and each case is unique, but there is a common theme. Many supervisors and managers have technical backgrounds that rarely focus on the financial aspects of running a lab. They have not been trained to recognize that improvements in processes are not just another expense. Such process improvements are an investment that resides in another location on the company’s balance sheet. We will consider a case study from chromatography laboratories to illustrate this idea.

Why don’t more laboratories make an effort to fix these situations? Today’s laboratories face many challenges, and each case is unique, but there is a common theme. Many supervisors and managers have technical backgrounds that rarely focus on the financial aspects of running a lab. They have not been trained to recognize that improvements in processes are not just another expense. Such process improvements are an investment that resides in another location on the company’s balance sheet. We will consider a case study from chromatography laboratories to illustrate this idea.

Using smaller HPLC columns

High-performance liquid chromatography (HPLC) has become one of the most useful analytical tools in the modern laboratory. Since its development in the 1970s, the technique has matured into a necessary tool for laboratories in almost every industry, but especially in pharmaceuticals, food, chemicals, and petroleum. There are more than a dozen major and minor manufacturers, and literally hundreds of column choices. The equipment is expensive ($40,000 to $50,000 for a typical entry-level system) and requires the use of high-purity (HPLC-grade) solvents.

Acetonitrile, the most common solvent, costs about $350 for a 4-liter bottle (including shipping and other handling fees), or a little less than $0.09/mL. If you are using this solvent at 1 mL/min. for eight hours a day, over the course of a year you will use about 120 liters of this solvent and spend $10,500 on purchase costs alone. Note that chemical disposal costs are an additional expense that we won’t factor in at this point, but they are often similar to the purchase cost and add to the laboratory’s total costs of operation. Now, suppose that I told you that you could save about 50 percent of those acetonitrile (and other HPLC solvent) costs by changing to a different column. Would you be interested?

Column manufacturers have made numerous improvements over the past 15 years. In addition to new phases with better stability, the suppliers have also been able to prepare identical columns with smaller diameters and shorter lengths. A smaller diameter means a smaller crosssectional area, and you need to push less mobile phase through the system to get the same flow velocity inside the column. As a result, you use less solvent.

A typical change might involve replacing a column with a 4.6 mm diameter with one that has a 3.0 mm diameter. The smaller column has about half the cross-sectional area of the original, so you could reduce your flow rate by about 50 percent. Using the above assumptions, your new solvent costs would be $5,250 a year, for an annual savings of $5,250. If you have a relatively modern instrument (less than 10 years old), you should be able to implement these changes with little or no modification of the equipment. Only a change in operating parameters is required.

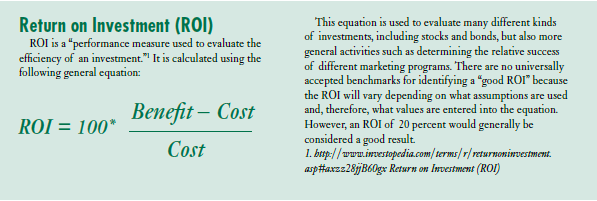

Calculating your ROI — a simple process change

As is always the case, nothing is free in the lab, so we will start by looking at making a simple change in column diameter for an existing method in a typical lab. To incorporate this change, it will require some additional time by a staff member to install the column, verify performance and/or make adjustments, evaluate real samples, and complete the documentation for the revised procedure. We will also assume that these activities require 40 hours of staff time and 40 hours of instrument time. Fully loaded costs for one staff member and an instrument together might be $100 an hour, which means the total internal cost is $4,000 to make this change. Using these estimates and the cost savings above, we can calculate the ROI as:

ROI = 100*(5,250 – 4,000)/4,000 = 31%.

This is a favorable result, and suggests that there is a longterm financial benefit to making this change. Yes, you will invest one staff member and one instrument for a week, but a year later your financial performance for this process will have been 30 percent better. Also, remember that we did not factor in disposal costs. With the new method, your disposal costs are also lower, which means another expense item is reduced and the actual ROI would be greater. In subsequent years your process continues to operate with this performance improvement, without the associated costs, providing added benefits from the investment.

Calculating your ROI — a more complex process change

Not every situation is so simple, so it is instructive to consider a somewhat more complicated scenario. Imagine that we have two instruments running a process similar to the one described above. Just implementing the above changes could save $10,500. However, suppose that you also want to minimize the overall use of this solvent by optimizing startup, equilibration, and other nonproductive usage activities, resulting in a further 10 percent reduction in use. Such a change will either increase overall capacity or reduce instrument “on” time. That is, you want to reduce your total use of acetonitrile by 60 percent, realizing a total savings of $6,300 for each system, or $12,600 for both systems.

This optimization is going to require an outside expert, because your staff does not have the time or expertise to do this kind of evaluation. The expert will cost about $6,700 to evaluate the process and recommend changes, assuming that the changes are relatively straightforward. However, this is a regulated lab (i.e., GMP-compliant), so additional staff time will be needed to validate the new method and complete the paperwork. This modification will require 20 hours of instrument and staff time (at $100 an hour total) to collect the data and another 40 hours of staff time (at $50 an hour) to write the reports and process the paperwork. The total costs are $10,700, and the ROI is:

ROI = 100*(12,600 – 10,700)/10,700 = 18%.

The ROI is not as favorable as the simple example, but this is a more complex situation with more demanding requirements and additional costs for the regulatory issues. Still, the number is positive, and it does not include other savings such as reduced disposal costs. These improvements continue into the future, but without the substantial investment of the first year, so the benefits are significantly larger.

Other applications

HPLC is not the only place where significant savings can be realized. Capillary gas chromatography operates under similar rules. Helium is the most common carrier gas, but it is a nonrenewable resource and the world’s known supplies are running out. As expected, costs are already rising at a rapid rate.

There are several different column diameters available from all manufacturers, and the savings are just as dramatic as in HPLC. If you reduce your column diameter from 0.32 mm to 0.25 mm, your helium usage can decrease by about 40 percent. If you are using 0.53 mm columns now, the reduction is almost 80 percent when changing to a smaller column.

Although these examples are specific to chromatography-based methods, it is important to note that this general approach can be applied in many other instrument types and processes as well. Improvements in efficiency and reduced operating costs are almost always possible if you are willing to make the investment. The ROI calculations can then be your guide to deciding which investments are the best choices for your laboratory.

Conclusion

Today’s laboratories are under stress from many directions, and there is constant pressure to be more profitable. However, we should not assume that the only way to be more profitable is to simply reduce existing expenses. With continuing advances in laboratory technologies, it is possible to improve both time and expense costs by upgrading to more contemporary technologies or even just training your staff how to use them. You do not have to choose the most expensive, or even the most recent, option, but you should evaluate the potential benefits and costs by calculating ROI for the investment.

Calculating ROI for laboratory activities is not common today, but mostly because many lab managers are not familiar with the idea. They have been trained in the technical requirements of the job, not the financial aspects. ROI is a common way to evaluate any business activity, and this approach is recognized as an appropriate tool even when applied to laboratory operations.

Our intent is not to suggest that such a simple strategy is appropriate for evaluating a complex multimillion-dollar project. Rather, we want to show laboratory managers how to look at their current systems and procedures and to give them a relatively simple tool for estimating the value from making improvements in the laboratory’s operations. Incorporating an ROI calculation into your proposal is going to give your ideas additional credibility because you are now speaking in the language that business managers and CFOs understand.

Dr. Merlin K. L. Bicking is president and senior analytical scientist of ACCTA, Inc., a company he founded in 1993. As a consulting analytical chemist, he provides technical problem solving and training to testing laboratories around the world. He has authored more than 20 publications and given more than 50 presentations at local, national, and international meetings in his 30 years of experience. Dr. Bicking holds a B.S. in chemistry from the University of Wisconsin-River Falls and a Ph.D. in organic-analytical chemistry from Iowa State University. He can be reached at mbicking@accta.com.

Thanks to Mr. Robert Zarracina, The Advisory Group Ltd., for helpful suggestions and comments.